Allied Market Research's report provided an estimation of the global orphan drugs market size estimated at $1,40,000.0 million in 2020 and is predicted to gain $4,35,686.3 million by 2030, exhibiting a CAGR of 11.8% during the forecast timeframe. The report offers a comprehensive outline of the leading investment pockets, the most successful strategies, the market dynamics, the market size and projections, the competitive analysis, and the forecast timeframe. This market report is an invaluable ... moreAllied Market Research's report provided an estimation of the global orphan drugs market size estimated at $1,40,000.0 million in 2020 and is predicted to gain $4,35,686.3 million by 2030, exhibiting a CAGR of 11.8% during the forecast timeframe. The report offers a comprehensive outline of the leading investment pockets, the most successful strategies, the market dynamics, the market size and projections, the competitive analysis, and the forecast timeframe. This market report is an invaluable resource for the leading players, new market entrants, and stakeholders in strategic planning and strengthening their competitive edge.

Recent Developments in the Orphan Drugs Market

High prices of orphan drugs are one of the major trends in the Orphan Drugs Market and are expected to increase further due to factors such as ageing population and increased R&D expenses. Around 40% of the Orphan Drugs cost more than $100,000 annually. However, growing awareness and the potential benefits regarding to orphan drugs coupled with the recent orphan drug approvals also acts as key trend and driver in the orphan drugs industry. Further, as per the recent trend in sales of orphan drugs from companies such as Johnson & Johnson’s multiple myeloma drug Darzalex and AstraZeneca’s Lynparza & Calquence, oncology will occupy most market share currently and in the coming years. These drugs together have generated an estimated revenue of around USD 25 Billion in 2022.

The report provides an in-depth assessment of the global orphan drugs market segmented on the basis of disease type, and region. It is presented in both tabular and graphical form, allowing investors and industry-leading players to gain insight into the most lucrative and rapidly expanding segments.

By disease type, the oncologic diseases segment held the major share in 2020, contributing to more than one-third of the global orphan drugs market. However, the metabolic diseases segment would showcase the fastest CAGR of 13.8% throughout the forecast timeframe.

The global orphan drugs market is divided into several geographical regions, including North America, Europe, Asia-Pacific (APAC), and LAMEA. The North America region accounted for the largest share in 2020, holding more than one-third of the global orphan drugs market. On the other hand, the Asia-Pacific region is projected to witness the fastest CAGR of 12.6% throughout the forecast timeframe.

The global orphan drugs market report has recognized several prominent players in the industry, including the following: Sanofi S.A., F. Hoffmann-La Roche Ltd., Novartis International AG, Amgen Inc., Bristol Myers Squibb, AbbVie Inc., Johnson & Johnson, GlaxoSmithKline plc., Pfizer Inc., and Amryt Pharma PLC. The industry players have also adopted various strategies, inclusive of collaborations, technological developments, expansions, and joint alliances to strengthen their position in the industry. This report provides an overview of the performance and growth of the leading players in the market.

Cardiovascular diseases remain the leading cause of death globally, and accurate diagnosis is critical to effective treatment. Electrophysiology (EP) is a specialized branch of cardiology that focuses on the electrical activity of the heart. By identifying and treating abnormal rhythms (arrhythmias), electrophysiology helps restore a healthy heartbeat—often without the need for open-heart surgery.

The global electrophysiology market size was valued at $6,499.7 million in 2020, and is projected ... moreCardiovascular diseases remain the leading cause of death globally, and accurate diagnosis is critical to effective treatment. Electrophysiology (EP) is a specialized branch of cardiology that focuses on the electrical activity of the heart. By identifying and treating abnormal rhythms (arrhythmias), electrophysiology helps restore a healthy heartbeat—often without the need for open-heart surgery.

The global electrophysiology market size was valued at $6,499.7 million in 2020, and is projected to reach $22,651.4 million by 2030, registering a CAGR of 14.4% from 2021 to 2030.

What is Electrophysiology?

Electrophysiology refers to the study and evaluation of the electrical impulses that regulate heartbeats. When these impulses misfire, it can lead to arrhythmias such as atrial fibrillation, tachycardia, or bradycardia. EP procedures help diagnose these irregularities and guide interventions like ablation therapy or pacemaker implantation.

Key Electrophysiology Procedures

Electrophysiology Study (EPS):

A minimally invasive test that maps the heart’s electrical signals using catheters.

Catheter Ablation:

Uses heat or cold energy to destroy small areas of heart tissue causing arrhythmias.

Pacemaker Implantation:

A small device implanted under the skin to help regulate slow heart rhythms.

Implantable Cardioverter Defibrillator (ICD):

Monitors and corrects life-threatening arrhythmias by delivering electric shocks.

Cryoablation and Radiofrequency Ablation:

Advanced forms of ablation therapy targeting specific problem areas in the heart.

Common Conditions Diagnosed or Treated

Atrial fibrillation (AFib)

Supraventricular tachycardia (SVT)

Ventricular tachycardia (VT)

Heart block or conduction disorders

Syncope (unexplained fainting)

Benefits of Electrophysiology

Minimally invasive diagnostics and treatments

High accuracy in pinpointing electrical disruptions

Improved patient outcomes and quality of life

Reduced reliance on long-term medications

Lower risk of stroke and cardiac arrest from untreated arrhythmias

Conclusion

Electrophysiology is revolutionizing how we diagnose and treat heart rhythm disorders. With faster, safer, and more precise interventions, EP is helping millions reclaim their heart health. As technologies continue to advance, the field will play an even greater role in preventive, personalized, and precision cardiology.

Introduction

In a world where rapid, accurate medical decisions are critical, Point of Care (POC) diagnostics are changing the game. These innovative tools bring laboratory testing closer to the patient - whether at the bedside, in the doctor's office, or even in remote locations. As demand for faster diagnosis and decentralized healthcare grows, POC diagnostics are becoming a cornerstone of modern medicine.

The global Point of Care Diagnostics Market Size was valued at $29,478.63 million in 2... moreIntroduction

In a world where rapid, accurate medical decisions are critical, Point of Care (POC) diagnostics are changing the game. These innovative tools bring laboratory testing closer to the patient - whether at the bedside, in the doctor's office, or even in remote locations. As demand for faster diagnosis and decentralized healthcare grows, POC diagnostics are becoming a cornerstone of modern medicine.

The global Point of Care Diagnostics Market Size was valued at $29,478.63 million in 2020 and is projected to reach $55,275.73 million by 2030, growing at a CAGR of 6.5% from 2021 to 2030.

What Are Point of Care Diagnostics?

Point of Care diagnostics refer to medical tests conducted near or at the site of patient care, without the need for centralized laboratory equipment. These tests deliver results within minutes, enabling immediate clinical decisions and improving outcomes, especially in emergency, rural, and primary care settings.

Key Features of POC Diagnostic Devices

Portability: Compact, handheld, or benchtop devices for easy use.

Speed: Most results are available in 5–30 minutes.

User-Friendliness: Minimal training required for operation.

Data Connectivity: Integration with electronic medical records (EMRs).

Accuracy: Comparable to lab-based diagnostics in many cases.

Common Applications of POC Diagnostics

Infectious Disease Testing

COVID-19, HIV, malaria, flu, and strep tests.

Chronic Disease Management

Glucose monitoring, lipid profiles, and HbA1c testing for diabetes.

Cardiac Markers

Troponin and BNP testing for rapid diagnosis of heart attacks or failure.

Pregnancy and Fertility Testing

Urine-based or serum tests for quick results.

Blood Gas and Electrolyte Analysis

Critical in ICUs and emergency departments.

Benefits of Point of Care Diagnostics

Faster Decision Making

Accelerates diagnosis and treatment, especially in time-sensitive conditions.

Improved Patient Outcomes

Early intervention leads to better prognosis and reduced complications.

Enhanced Accessibility

Useful in rural or resource-limited settings where lab infrastructure is minimal.

Reduced Healthcare Costs

Fewer lab referrals and shorter hospital stays can lower overall expenses.

Patient Empowerment

Home-use POC devices like glucose meters allow for self-monitoring and better disease control.

Market Insights and Growth Drivers

The global point of care diagnostics market is booming, driven by:

Rising prevalence of chronic and infectious diseases

Need for rapid diagnostics in emergency and pandemic settings

Growth of home healthcare and telemedicine

Technological innovations like biosensors, microfluidics, and smartphone-based diagnostics

The market is particularly strong in North America and Europe, with Asia-Pacific experiencing rapid adoption due to improving healthcare access.

Challenges in POC Adoption

Regulatory approvals and quality control

Data security and integration with existing healthcare systems

Limited test menus compared to centralized labs

Risk of misinterpretation by non-clinical users in home settings

Future Trends in Point of Care Diagnostics

AI-integrated diagnostic platforms

Wearable and continuous monitoring devices

Lab-on-a-chip (LOC) technologies

Expansion of multiplex testing (multiple analytes in one test)

Sustainable and disposable test formats

Conclusion

Point of Care diagnostics are reshaping the future of healthcare by delivering fast, reliable, and accessible testing solutions. As technology continues to advance and the demand for patient-centric care increases, POC diagnostics will play an even greater role in improving clinical outcomes and reducing healthcare disparities worldwide.

Introduction

In the ever-evolving world of diagnostic medicine, hematology analyzers play a critical role in identifying and monitoring a wide range of health conditions. These advanced instruments provide quick, reliable, and comprehensive blood analysis — making them essential tools in clinical laboratories, hospitals, and research centers worldwide.

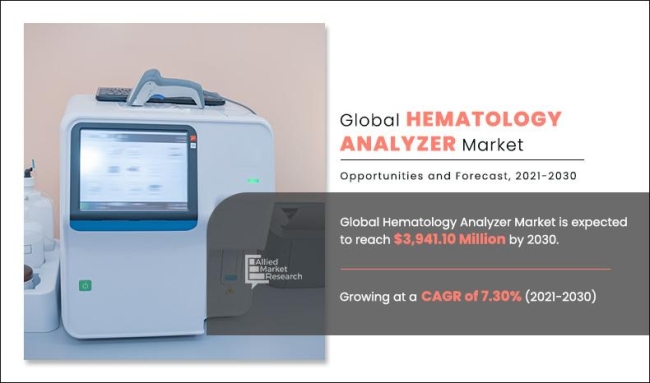

The global hematology analyzer market size was valued at $1,962.40 million in 2020 and is projected to reach $3,941.10 million by 2030 registe... moreIntroduction

In the ever-evolving world of diagnostic medicine, hematology analyzers play a critical role in identifying and monitoring a wide range of health conditions. These advanced instruments provide quick, reliable, and comprehensive blood analysis — making them essential tools in clinical laboratories, hospitals, and research centers worldwide.

The global hematology analyzer market size was valued at $1,962.40 million in 2020 and is projected to reach $3,941.10 million by 2030 registering a CAGR of 7.30% from 2021 to 2030.

What Is a Hematology Analyzer?

A hematology analyzer is an automated machine designed to count and characterize blood cells, primarily red blood cells (RBCs), white blood cells (WBCs), and platelets. It helps in generating complete blood count (CBC) reports, which are crucial in detecting infections, anemia, leukemia, clotting disorders, and other hematologic abnormalities.

Key Features of Hematology Analyzers

Automated Cell Counting

Enables accurate and fast enumeration of various blood cell types.

Differential White Cell Count

Classifies WBCs into subtypes such as neutrophils, lymphocytes, monocytes, etc.

Hemoglobin Measurement

Essential in diagnosing anemia and evaluating oxygen-carrying capacity.

Flagging Abnormal Results

Alerts technicians to potential issues like immature or irregular cells.

User-Friendly Interface

Touchscreen displays, data management systems, and connectivity options.

Types of Hematology Analyzers

3-Part Differential Analyzer

Differentiates WBCs into 3 groups: lymphocytes, monocytes, and granulocytes. Suitable for smaller labs.

5-Part Differential Analyzer

Offers detailed classification of WBCs and higher accuracy. Common in hospitals and reference labs.

High-End Analyzers

Include additional parameters like reticulocyte count, nucleated RBCs, and flow cytometry capabilities.

Applications in Healthcare

Hematology analyzers are used for:

Routine health check-ups

Diagnosing blood disorders (e.g., leukemia, anemia)

Monitoring infection or inflammation

Post-surgical and chemotherapy monitoring

Blood donation screening

Market Growth and Trends

The global hematology analyzer market is experiencing significant growth, driven by:

Rising prevalence of blood disorders and infectious diseases

Increasing demand for automated diagnostic solutions

Expansion of point-of-care testing in rural and low-resource settings

Integration of AI and machine learning for improved diagnostics

Regions like North America, Europe, and Asia-Pacific are leading in adoption, with the Asia-Pacific market projected to grow fastest due to improving healthcare infrastructure.

Challenges in the Market

High equipment costs for advanced models

Training requirements for lab personnel

Maintenance and calibration needs

Limited accessibility in underdeveloped regions

The Future of Hematology Analyzers

Technological advancements are shaping the next generation of hematology analyzers with features like:

Real-time connectivity with lab information systems (LIS

Compact and portable designs for remote diagnostics

Enhanced sensitivity for early disease detection

Automation and AI-driven interpretation

Conclusion

Hematology analyzers are indispensable in modern diagnostics, offering fast, accurate, and detailed blood analysis. As technology continues to evolve, these devices will become more accessible and efficient — enabling earlier detection, better disease management, and improved patient care across the globe.

Introduction

Medical device packaging plays a crucial role in the healthcare supply chain, serving not just as a container, but as a safeguard for product sterility, integrity, and usability. As global demand for medical devices grows, so does the need for reliable, regulation-compliant packaging that can withstand harsh environments and preserve product performance until point-of-use.

The global medical device packaging market size was valued at $ 22,097.10 Million in 2020, and is projected t... moreIntroduction

Medical device packaging plays a crucial role in the healthcare supply chain, serving not just as a container, but as a safeguard for product sterility, integrity, and usability. As global demand for medical devices grows, so does the need for reliable, regulation-compliant packaging that can withstand harsh environments and preserve product performance until point-of-use.

The global medical device packaging market size was valued at $ 22,097.10 Million in 2020, and is projected to reach $ 47,117.70 Million by 2030 registering a CAGR of 7.50% from 2021 to 2030.

What is Medical Device Packaging?

Medical device packaging refers to the materials and methods used to protect medical devices during transportation, storage, and handling. This packaging must ensure sterility, durability, and compliance with health regulations, while also providing user-friendly access for healthcare professionals.

Key Functions of Medical Device Packaging

Protection from Contamination:

Ensures devices remain sterile and free from bacteria or particulates.

Mechanical Protection:

Shields delicate components from physical damage during transport or storage.

Barrier Properties:

Prevents exposure to moisture, light, oxygen, or chemicals.

User Safety & Convenience:

Includes clear labeling, easy-open features, and usage instructions.

Regulatory Compliance:

Meets FDA, ISO, and other regional guidelines for sterile barrier systems.

Common Packaging Materials

Tyvek®: Durable and breathable, ideal for sterilizable pouches and lids.

Medical-grade Paper: Cost-effective and often used for sterile barrier systems.

Plastics (PET, PVC, PE): Used in trays, pouches, and rigid containers.

Foil Laminates: Provide moisture and oxygen barrier for sensitive devices.

Blister Packaging: Transparent, sealed cavities ideal for single-use devices.

Types of Medical Device Packaging

Pouches & Bags — For lightweight, single-use items.

Blister Packs — Enable visual inspection while maintaining sterility.

Shrink Wraps & Overwraps — Secondary protection during distribution.

Labels & Inserts — Provide usage instructions, compliance info, and barcodes.

Key Market Drivers

Rising demand for sterile and disposable devices

Stringent regulatory requirements (FDA, ISO 11607)

Growth in home healthcare and point-of-care diagnostics

Focus on anti-counterfeiting and traceability (UDI labels)

Sustainability trends pushing for eco-friendly packaging solutions

Market Outlook

The global medical device packaging market is projected to witness steady growth, fueled by increased R&D, higher surgical volumes, and regulatory pressure. North America leads in market share, while Asia-Pacific is expected to show the fastest growth due to expanding healthcare infrastructure.

Challenges in Medical Device Packaging

Complex regulatory approvals and validations

Balancing cost-efficiency with performance

Developing recyclable and sustainable materials

Ensuring tamper evidence and counterfeiting prevention

Future Trends

Smart Packaging with RFID/NFC for real-time tracking

Sustainable Packaging with biodegradable and recyclable materials

Automation & AI in packaging line operation

Personalized Packaging for custom surgical kits and 3D-printed devices

Conclusion

Medical device packaging is more than just a wrap — it’s a critical element that ensures product quality, user safety, and regulatory compliance. As innovation continues to reshape the healthcare landscape, packaging solutions must evolve to meet the demands of tomorrow’s medical technologies.

Chronic pain affects millions worldwide, diminishing quality of life and creating long-term healthcare burdens. To combat this, pain management devices have emerged as effective, drug-free alternatives or supplements to traditional treatments. From wearable stimulators to implantable systems, these devices are transforming how we address both acute and chronic pain.

The global pain management devices market size was valued at $3,689.20 million in 2020, and is projected to reach $5... moreIntroduction

Chronic pain affects millions worldwide, diminishing quality of life and creating long-term healthcare burdens. To combat this, pain management devices have emerged as effective, drug-free alternatives or supplements to traditional treatments. From wearable stimulators to implantable systems, these devices are transforming how we address both acute and chronic pain.

The global pain management devices market size was valued at $3,689.20 million in 2020, and is projected to reach $5,767.69 million by 2028, registering a CAGR of 6.3% from 2021 to 2028.

What Are Pain Management Devices?

Pain management devices are medical technologies designed to alleviate pain through electrical stimulation, heat therapy, or drug delivery mechanisms. They provide targeted relief, often reducing or eliminating the need for long-term medication use, especially opioids.

Common Types of Pain Management Devices

Transcutaneous Electrical Nerve Stimulation (TENS):

Sends low-voltage electrical currents to nerves, blocking pain signals.

Neurostimulation Devices (Spinal Cord Stimulators):

Implanted near the spine, these deliver electrical impulses to disrupt pain perception.

Infusion Pumps:

Deliver pain-relieving medication directly into the bloodstream or spinal fluid.

Radiofrequency Ablation Devices:

Use heat generated by radio waves to disrupt nerve function temporarily.

Cryotherapy Devices:

Apply localized cold treatment to numb pain and reduce inflammation.

Applications in Healthcare

Pain management devices are used in the treatment of:

Chronic back and neck pain

Cancer-related pai

Post-surgical pain

Arthritis and joint disorders

Neuropathic pain (e.g., diabetic neuropathy)

Key Benefits

Non-invasive or minimally invasive solutions

Reduced reliance on opioids

Faster recovery and improved mobility

Customizable therapy options

Fewer side effects than pharmacological alternatives

Market Insights & Growth Drivers

The global pain management devices market is expanding rapidly, driven by:

Rising cases of chronic conditions and post-operative pain

Growing preference for non-opioid pain therapies

Technological advancements in wearable and wireless devices

Increasing geriatric population globally

According to industry reports, the market is expected to witness substantial growth over the next decade, particularly in North America and Asia-Pacific regions.

Challenges in Adoption

Despite their benefits, pain management devices face certain barriers:

High cost of advanced systems

Reimbursement limitations in some regions

Risk of infection or device malfunction (for implantables)

Patient hesitancy or lack of awareness

The Future of Pain Relief

Innovations such as AI-enabled wearable stimulators, mobile app integration, and personalized therapy platforms are set to redefine pain management. With the healthcare industry emphasizing value-based care, these devices will play a crucial role in improving outcomes while reducing costs.

Conclusion

Pain management devices offer a promising path to long-term relief without the risks of opioid dependency. As technology advances and awareness grows, these devices will continue to empower patients to live healthier, pain-free lives.

In today’s rapidly advancing medical landscape, precision and minimally invasive approaches are becoming the cornerstones of modern surgery. One of the key technologies enabling this transformation is the Surgical Navigation System (SNS). Often referred to as the “GPS for surgeons,” these systems provide real-time, 3D guidance, helping clinicians navigate complex anatomical structures with accuracy and confidence.

The global surgical navigation systems market size was valued at ... more

Introduction

In today’s rapidly advancing medical landscape, precision and minimally invasive approaches are becoming the cornerstones of modern surgery. One of the key technologies enabling this transformation is the Surgical Navigation System (SNS). Often referred to as the “GPS for surgeons,” these systems provide real-time, 3D guidance, helping clinicians navigate complex anatomical structures with accuracy and confidence.

The global surgical navigation systems market size was valued at $940.68 Million in 2020, and is projected to reach $1,755.67 Million by 2030, registering a CAGR of 6.4% from 2021 to 2030.

What Are Surgical Navigation Systems?

Surgical navigation systems are computer-assisted platforms that integrate preoperative imaging (CT, MRI) with intraoperative tracking technologies to guide surgical instruments in real-time. These systems enhance the surgeon’s spatial awareness and allow for precise targeting of tissues or lesions while minimizing damage to surrounding healthy structures.

Key Components of Surgical Navigation Systems

Imaging Software: Integrates patient data from scans to create detailed 3D anatomical maps.

Tracking Technology: Uses infrared cameras or electromagnetic sensors to track instrument location.

Display Units: Provides visual feedback for accurate movement and placement during surgery.

Calibration Tools: Ensures that the system’s guidance is aligned with the actual patient anatomy.

Applications in Modern Surgery

Surgical navigation systems are increasingly used across several specialties:

Neurosurgery: For tumor resections, spinal fusions, and epilepsy procedures.

Orthopedics: In joint replacements and fracture fixations.

ENT Surgery: For sinus surgery and skull base operations.

Spine Surgery: Helps navigate vertebrae and avoid nerve damage.

Oncology: Assists in removing tumors with minimal impact on healthy tissue.

Benefits of Surgical Navigation

Increased Accuracy: Reduces human error by guiding instruments to precise locations.

Minimally Invasive: Supports smaller incisions, leading to faster recovery times.

Reduced Operating Time: Streamlines surgical planning and execution.

Improved Outcomes: Enhances surgical confidence and patient safety.

Market Outlook and Innovations

The global surgical navigation system market is projected to grow significantly, driven by rising demand for minimally invasive procedures, aging populations, and technological innovations like AI-powered navigation, robotic-assisted surgery, and augmented reality (AR) integration.

Challenges and Considerations

Despite its advantages, some challenges include:

High initial investment and maintenance costs

Learning curve for surgeons unfamiliar with the technology

Limited integration in low-resource healthcare settings

Conclusion

Surgical navigation systems are revolutionizing how surgeries are performed by offering a level of precision that was once unattainable. As technology continues to evolve, these systems are poised to become an essential part of operating rooms worldwide, leading to safer procedures, better outcomes, and enhanced surgeon capabilities.

A comprehensive study of Industry Dynamics and Competitive Landscape in the Bispecific Antibody Industry From 2023 to 2032

Allied Market Research published a report on the bispecific antibody market, which includes a detailed study of the competitive landscape and regional analysis. This report also provides information about industry dynamics, which includes opportunities, challenges, and growth drivers. The global bispecific antibody industry accounted for $5.5 billion in 2022 and is expected... moreA comprehensive study of Industry Dynamics and Competitive Landscape in the Bispecific Antibody Industry From 2023 to 2032

Allied Market Research published a report on the bispecific antibody market, which includes a detailed study of the competitive landscape and regional analysis. This report also provides information about industry dynamics, which includes opportunities, challenges, and growth drivers. The global bispecific antibody industry accounted for $5.5 billion in 2022 and is expected to grow to $109.4 billion by 2032, reaching a CAGR of 34.8% from 2023 to 2032.

Key industry players

Amgen Inc., Pfizer Ltd

Bristol-Myers Squibb Company

Merus

AbbVie Inc

Johnson & Johnson

F. Hoffmann-La Roche Ltd.

Regeneron Pharmaceuticals, Inc.

MacroGenics Inc.

AstraZeneca plc

Important questions and answers

Which are the leading companies in the bispecific antibody industry?

What is the fastest-growing region in this sector?

What are the key trends in this domain?

Which is the base year calculated in the bispecific antibody industry?

How many bispecific antibody companies are profiled in the report?

Growth drivers

The growing number of cancer and autoimmune disease increases the need for new treatment options, which surges the importance of bispecific antibodies in treating conditions with limited medical options. Cancer and autoimmune diseases create major difficulties for both patients and healthcare systems around the world, leading to a strong need for better treatments. Bispecific antibodies offer a promising option as they target two different disease markers simultaneously, which makes treatment more effective.

The bispecific antibodies industry is expected to grow quickly by the advancements in immune system research and improvements in biotechnology. One of the main reasons for this growth is increasing use of bispecific antibodies in cancer treatment. These new treatments are designed to specifically target different types of cancer, which is likely to help patients to feel better and recover faster. Bispecific antibodies are helpful for not only cancer but are also used to treat other health problems such as infectious diseases, neurodegenerative disorders, and autoimmune diseases. Their ability to target more than one disease pathways makes them a strong option for treating different health conditions.

Partnerships and collaborations between academic institutions, pharmaceutical companies, and biotechnology firms are supporting the growth of bispecific antibodies in healthcare. These partnerships and collaborations utilize different strengths and resources to discover new treatments effectively.

Regional analysis

The bispecific antibody industry in North America is expected to grow in the coming years, with rise in cancer cases due to lifestyle changes such as a lack of physical activity and smoking. Also, many companies in the region are involved in making bispecific antibodies, which contribute to the growth of this industry. Moreover, the Asia-Pacific region is also expected to grow in the coming years due to the rise in chronic diseases such as autoimmune diseases and cancer. This factor drives the demand for bispecific antibodies for treatment purposes, which boosts the growth of the industry.

Recent developments

In January 2025, Biocytogen announced a partnership with Acepodia to jointly analyze a dual payload bispecific antibody-drug conjugate (BSAD2C) program. This partnership combines Biocytogen’s RenLite platform and Acepodia’s AD2C technology to address major challenges in cancer treatment, like drug resistance and tumor heterogeneity.

In October 2024, ImmunoPrecise announced a partnership with Biotheus on bispecific antibodies to treat cancer. The agreement aims to develop a new bispecific antibody treatment for hypoxic solid tumors, using Talem Therapeutics’ lead drug candidate, TATX-20.

Conclusion

In summary, the AMR report provides an in-depth analysis of industry dynamics, including opportunities, challenges, and growth drivers. This report also offers an overview of industry segmentation and a competitive landscape, which is expected to help industry leaders and stakeholders in strategic decision-making and analyzing industry trends.